Why Require an Insurance Inspection?

Ron Uline, Head of Risk & Inspection

June 7th 2022

As an insurance underwriter, an important factor in your decision-making regarding whether or not to offer a particular policy, and at what price, may hinge on the results of an insurance inspection.

Whenever an item or individual is being considered for insurance coverage, a first-hand inspection can be a necessary part of the process. An insurance policy covering expensive jewelry items, for example, may require an eyes-on inspection by a jewelry expert to ensure that the actual value of the jewels being considered for coverage matches what the proposed insured claims.

An Insurance Inspection for Every Policy

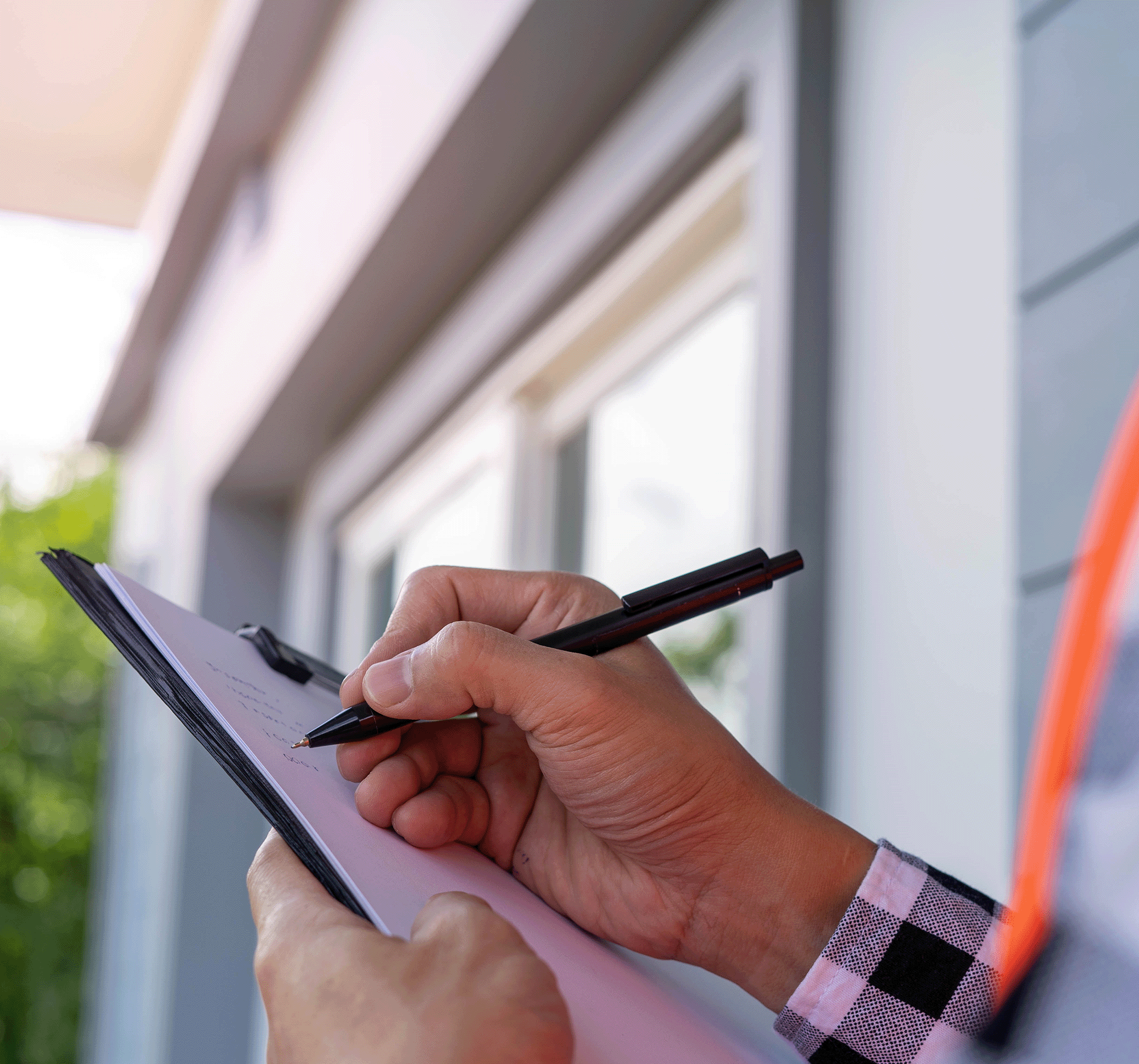

As a rule, the consideration for every insurance policy will call for some type of inspection. Different levels of inspections may be conducted. For a homeowners’ policy, the on-site inspection may be as simple as a cursory drive-by to verify address, location, and occupancy type. Or it may be involved enough to require a professional home inspector to spend a number of hours studying the home, both inside and out, to determine the exact condition of the residence, verify the information given by the homeowner on their application, and to uncover any potential problems with the home that could lead to future claims.

Someone applying for a life insurance policy can expect to be “inspected” by a medical professional and to submit to certain required tests to “inspect” their current health condition and status. Along with these physical inspections, a number of questions regarding everything from lifestyle to family history may be asked. These are all means of determining what kind of risk the potential insured presents and if a policy is granted, what a fair and accurate cost of the policy would be.

Insuring Mechanical Devices

Many insurance policies cover not only the value to replace an item if it were to become damaged or destroyed in an event covered by the policy, but also liabilities faced regarding the insured object. Many policies contain a liability component, whether it’s a policy covering an automobile, motorcycle, or a piece of machinery in a factory where a worker may potentially get injured.

Even your home, which may seem to be relatively benign liability-wise, will contain liability protection in its insurance coverage. If someone visiting your home trips and gets injured as a result of your damaged front porch or your dog bites them and they require medical treatment, your homeowners’ insurance policy’s liability section will likely cover you from financial loss. When a homeowners’ policy is being written, a thorough insurance inspection should have noted the damaged front porch or the potentially dangerous dog and the price charged for the policy should reflect these risks.

As a policy underwriter, you may require the homeowner to remedy the problem with the front porch before coverage is finalized. Also, many insurance companies exclude a number of dog breeds that have a known reputation for being dangerous. If you have one of their banned dog breeds in your household, you may be denied coverage altogether.

Paper Inspections

In addition to eyes-on physical inspections for use when underwriting an insurance policy, a whole raft of data is typically available to assist in the underwriting process. As an underwriter, the more pertinent data you have access to, the more able you will be to accurately assess risk and the fairer and more accurate your policy pricing will be.

When underwriting a homeowners’ insurance policy, applicable data is collected and plugged into the appropriate computer software program for a general comparison to other homeowners’ policies. Policy premiums are based on a number of factors, including:

- Property Location – this tells a good deal about the home’s risk. How likely is the home to experience a robbery, a flood, or a wildfire? How close are the nearest fire hydrants and stations?

- Property Construction Characteristics – age and construction of the home can tell how well it’s likely to withstand storms or other catastrophic events, especially in areas where there are frequent hurricanes, tornados, etc.

- Established Weather Patterns – chances of loss in an area can be impacted by rain, winds, tides, and storm patterns.

- Claims History – past claims that could have been prevented will be taken into account in policy pricing.

The Importance of Homeowners’ Policy Inspections

All insurance policy underwriting has a place for inspections of one type or another, and few require more detail than a home inspection for a home policy. A thorough home inspection will include everything from the foundation to the roof and all areas in between. Uncovering any and all risks will help identify the type and amount of coverage needed and appropriate pricing. Davies has been assisting insurers with top-notch inspections for decades and providing dedicated field underwriting support and accurate underwriting reports.

-

May 25th 2022

Claims Adjuster Time Techniques

Claims adjusters work for insurance companies, banks, and other firms to evaluate the…

-

August 17th 2021

Why are catastrophe (CAT) teams an identity and access risk?

While some insurance companies have full-time CAT teams, others use a variety of…

-

January 24th 2023

Four Key Takeaways from Florida’s Legislative Property Insurance Overhaul

There are new property insurance rules for Florida’s insurance carriers requiring elaborate document…